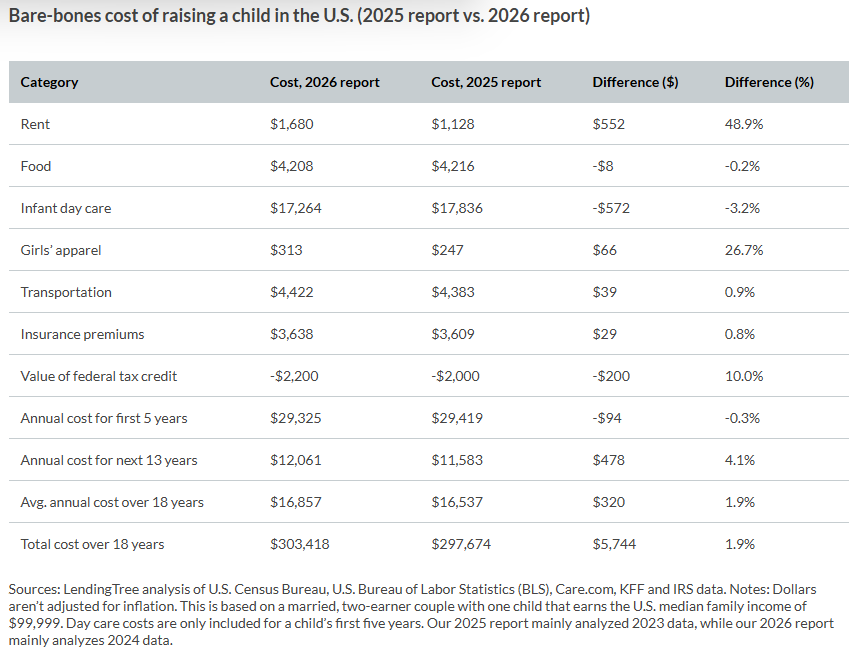

$303,418. That's the additional cost to raise one child over 18 years.

LendingTree’s 2026 analysis makes that visible. But here’s what matters more: the timing of when those costs hit—and how to position yourself financially if you’re in your 40s, either managing kids already or considering another.

Most women don’t connect the dots. Child-rearing costs peak during the exact years when perimenopause begins. It’s not a catastrophe. It’s a planning opportunity.

THE TIMELINE: WHAT YOU’RE ACTUALLY MANAGING

Understanding when costs hit changes how you prepare.

The average family spends $29,325 annually during a child’s first five years. That drops to $12,061 for the next 13 years. Manageable, if you know it’s coming.

But here’s the strategic detail most financial plans miss: if you’re 40 and your youngest is 10, or if you’re 42 and considering another child, you’re managing peak expenses during your peak earning years. That overlap is the planning point.

A 48-year-old partner at a consulting firm with a 12-year-old and aging parents is managing tuition, college planning, and caregiving simultaneously. She’s not overwhelmed—she’s aware. She knows these costs are real. And because she knows, she planned for them three years earlier.

That’s the move.

WHERE THE COSTS ACTUALLY HIT

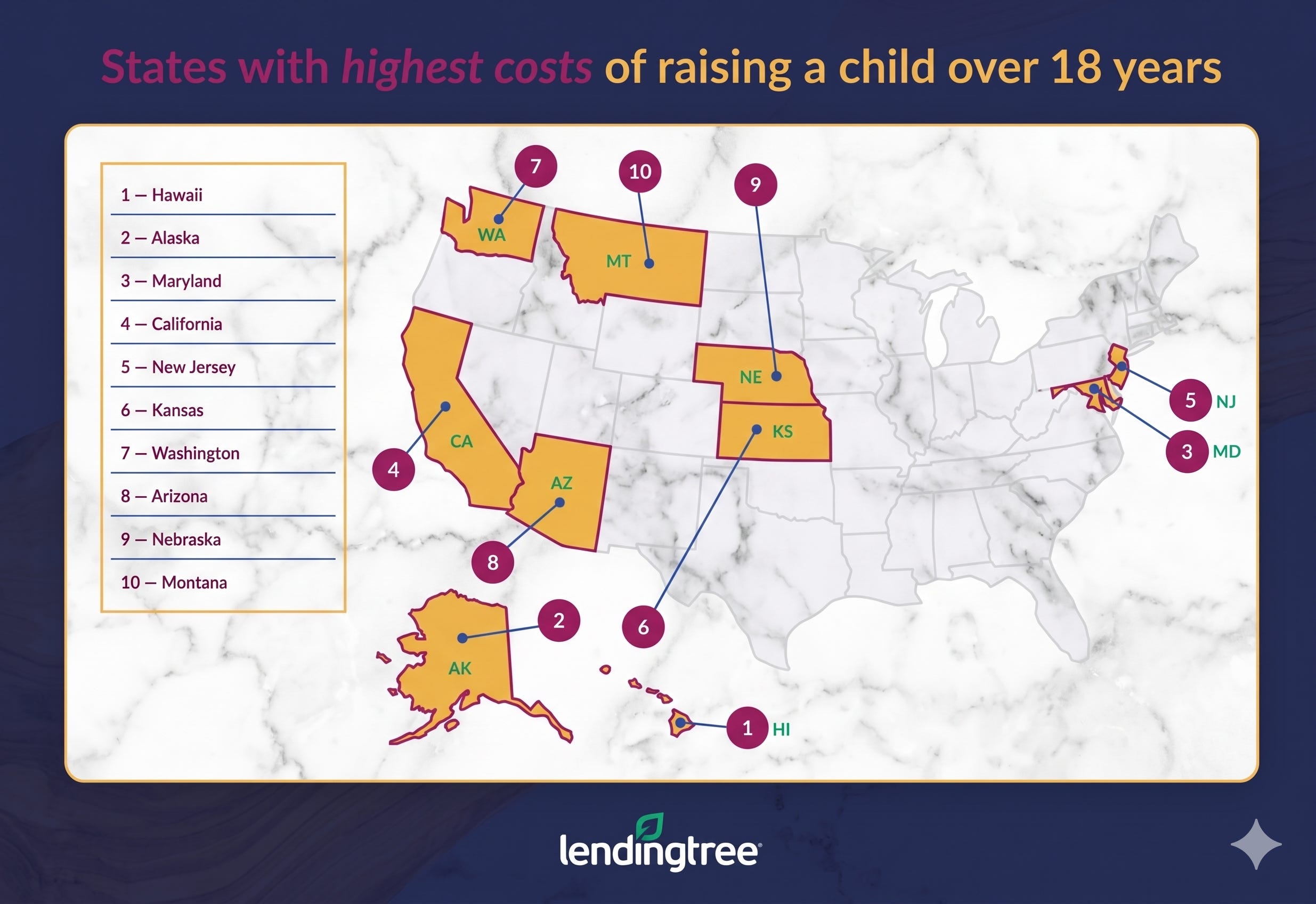

If you live in Hawaii, you're spending 27.4% of your income on child-related costs alone.

LendingTree found dramatic variance. Hawaii families spend $40,342 annually for ages 0-5. Mississippi families spend $17,148. That $23K gap compounds.

If you live in California ($33,692 annually), or you’re considering a move during your 40s, the cost structure changes your strategy. If you’re in Texas ($20,968 annually) or Florida ($24,968), your financial margin is wider.

Geography isn’t destiny. But it is a data point for planning. If you’re considering a move, or if you already live in a high-cost state, you now have the number. You can plan around it.

THE STRATEGIC WINDOW: AGES 40-55

This is when you position yourself financially and professionally.

Most women enter perimenopause in their mid-40s. Most children are in school-age expense years (ages 5-18) during a parent’s 40s-55. This window is where career advancement, earning momentum, and financial position are built—or stalled.

The clinical reality: perimenopause impacts sleep quality, cognitive function, and emotional regulation. For many high-performing women, managing symptoms while managing parenting costs requires deliberate planning, not heroics.

Here’s what that looks like in practice: A 42-year-old physician is managing a mortgage, two kids (ages 8 and 5), and entering early perimenopause. She has brain fog some mornings. She’s also a top earner in her practice. These two facts are not contradictory if she plans for both.

The women who navigate this successfully don’t white-knuckle through it. They anticipate the timeline and adjust their financial and professional strategy accordingly.

THREE MOVES TO PREPARE (WHETHER YOU HAVE KIDS NOW OR YOU’RE CONSIDERING)

Move 1: Map your actual costs against your earning timeline.

If you have kids already, you know the number now. If you’re considering another child, calculate what years 10-18 of that child look like for your life.

Your current child is in college at your age 48-55? That’s your peak earning opportunity window. That’s also your perimenopause window. Not a problem—but plan for it.

Ask yourself: What’s my financial position at 45 such that I can handle peak expenses at 48-55 without career compromise?

If the answer is “I need to accelerate earning or build passive income,” you now have 3-5 years to do it. If the answer is “I’m positioned fine,” you can move forward confidently.

Move 2: If you’re considering another child, factor in the full 18-year cost and your earning capacity timeline.

A woman at 42 considering a third child isn’t just budgeting for $303K. She’s budgeting for what her career and earning power look like at 50 (when that child is 8) and 60 (when that child is 18).

That’s the calculation. Not “Can I afford the kid?” but “Can I afford the kid while maintaining my earning trajectory?”

For many women, the answer is absolutely yes—if they plan for it. Negotiating higher base salary now, building side income, adjusting career timing, or shifting roles before peak expenses hit—these are strategic moves, not sacrifices.

Move 3: Audit your financial plan for perimenopause-specific gaps.

Most financial advisors plan for earning consistency across decades. You won’t have complete consistency during perimenopause (and that’s fine). But you can plan around it.

If you’re 40, your financial plan should have this checkpoint: “At 45-50, here’s what I’m prioritizing to ensure I’m positioned for ages 50-60.” That might be accelerating a promotion, building equity, or securing passive income.

Women who do this don’t feel derailed by perimenopause expenses. They feel prepared.

THE MOVE FORWARD

You can absolutely have children while managing perimenopause. The move is awareness + strategy, not fear.

If you have kids already and haven’t mapped your financial position against the next 5-10 years, now’s the time. If you’re considering another child, these numbers let you decide with actual data instead of guessing.

What does your 5-year financial and professional plan look like when you factor in both possibilities?

Share this with one woman who’s either managing kids already or weighing whether to have another. The numbers are less scary when you plan with them.