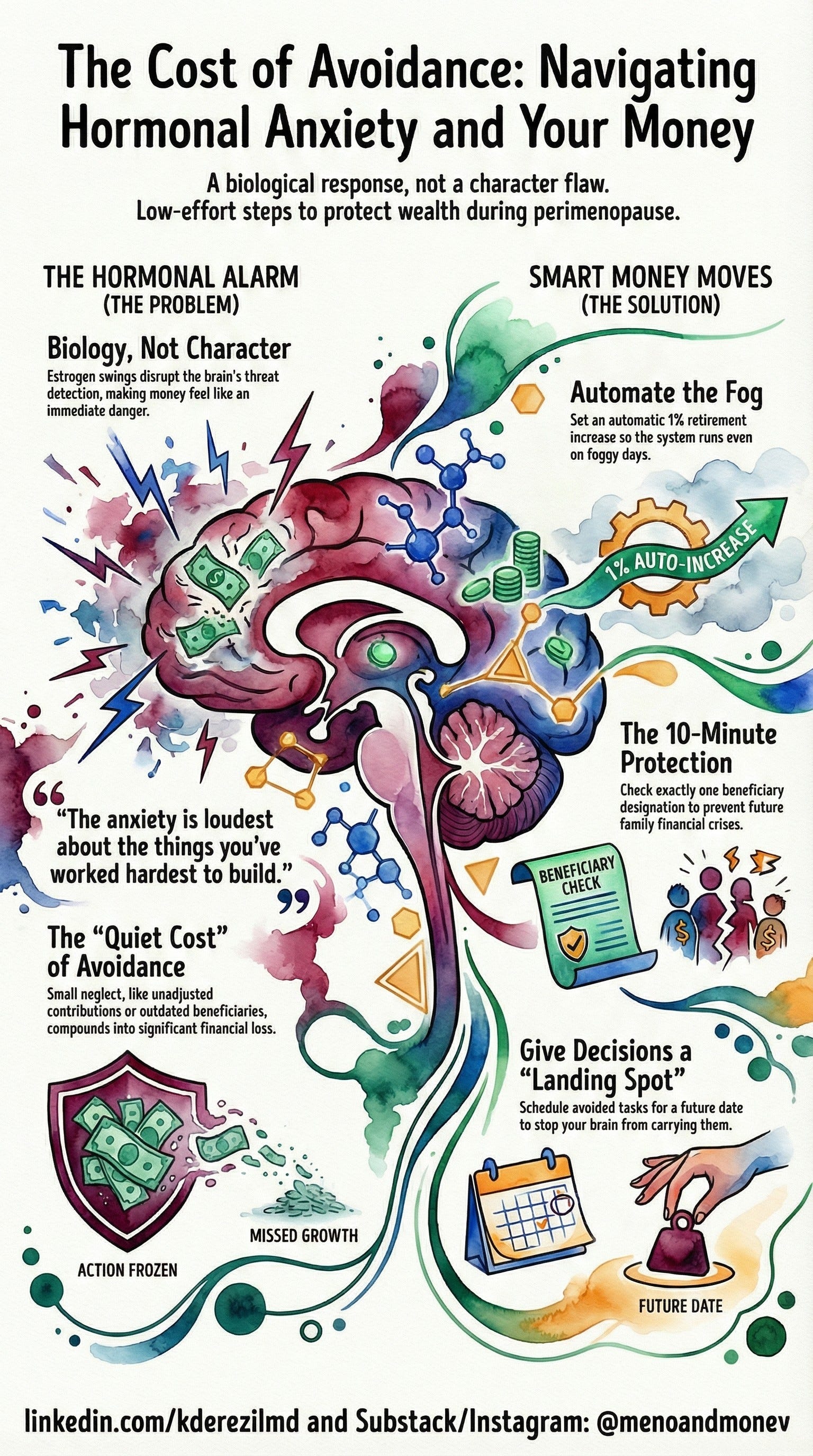

Why Does Avoiding Your Money Feel Safer—When Avoidance Is the Actual Risk?

You opened your retirement account last Tuesday. Stared at the balance. Felt a wave of dread—even though nothing had changed since last month.

Then you closed the app and went to bed.

The Tension

You’re not avoiding your finances because you’re irresponsible. You’re avoiding them because your brain is genuinely overwhelmed—and every time you try to engage, it sounds an alarm you can’t turn off.

That alarm feels like financial danger. It isn’t.

Myth: The anxiety you feel about money means something is financially wrong.

Reality: During perimenopause, estrogen swings directly disrupt the part of your brain that decides what’s a real threat and what isn’t. Your brain’s alarm system misfires. Money—because it feels concrete and controllable—becomes a lightning rod for that fear.

Research confirms this isn’t personality. It’s neuroscience. Studies from SWAN (one of the largest long-term studies on women’s health) found that anxiety spikes sharply in late perimenopause—even in women with no prior anxiety history. Your brain is working exactly as hormones are directing it to. That’s not a character flaw. That’s biology.

The financial risk isn’t the anxiety. It’s the avoidance the anxiety produces.

The Money Connection

Here’s what nobody says plainly: avoidance during your 40s and 50s is expensive.

Not dramatically. Quietly. It looks like beneficiary forms still listing an ex. A 401(k) contribution that hasn’t been adjusted in four years. A life insurance policy you meant to review. An FSA that expired unused.

Small neglect in peak earning years compounds. That’s the actual cost.

The anxiety feels like the problem. The frozen inaction is where the money goes.

Smart Money Moves

Make one thing automatic this week. Set up an automatic increase to your retirement contribution—even 1%. You don’t have to decide anything on a foggy day if the system is already running. Log in once, set it, leave.

Spend 10 minutes on one “protect future you” task. Check one beneficiary designation. Just one. Your 401(k), your life insurance, your bank account. One. This is the kind of thing that costs families tens of thousands of dollars when it’s wrong—and takes less than one calendar block to fix.

Name the decision you keep avoiding—then schedule it, not for today. Write it down. “Review insurance.” “Call HR about FMLA.” “Open the estate folder.” Put it on a calendar two weeks out, on a Saturday morning. You’re not solving it tonight. You’re just giving it a landing spot so your brain stops carrying it.

You don’t have to solve this tonight.

You just have to stop letting the alarm convince you there’s nothing worth protecting.

“The anxiety is loudest about the things you’ve worked hardest to build.”

One question: What’s the one financial task you keep moving to next week? Reply with the actual thing—even if it’s just one word.

Know someone who said “I just can’t think lately”? Forward this to her. She’s probably not being dramatic. She’s probably in the window.

This doesn’t mean you’re failing. It means you’re in the hardest part—and you still showed up to read this.