Retirement Now Requires $2 Million — and Most Women in Perimenopause Aren’t Even Close

You keep telling yourself you’ll deal with the retirement account after the hot flashes slow down. After the sleep evens out. After this season at work gets less intense.

Here’s the part nobody says out loud: that wait has a price tag.

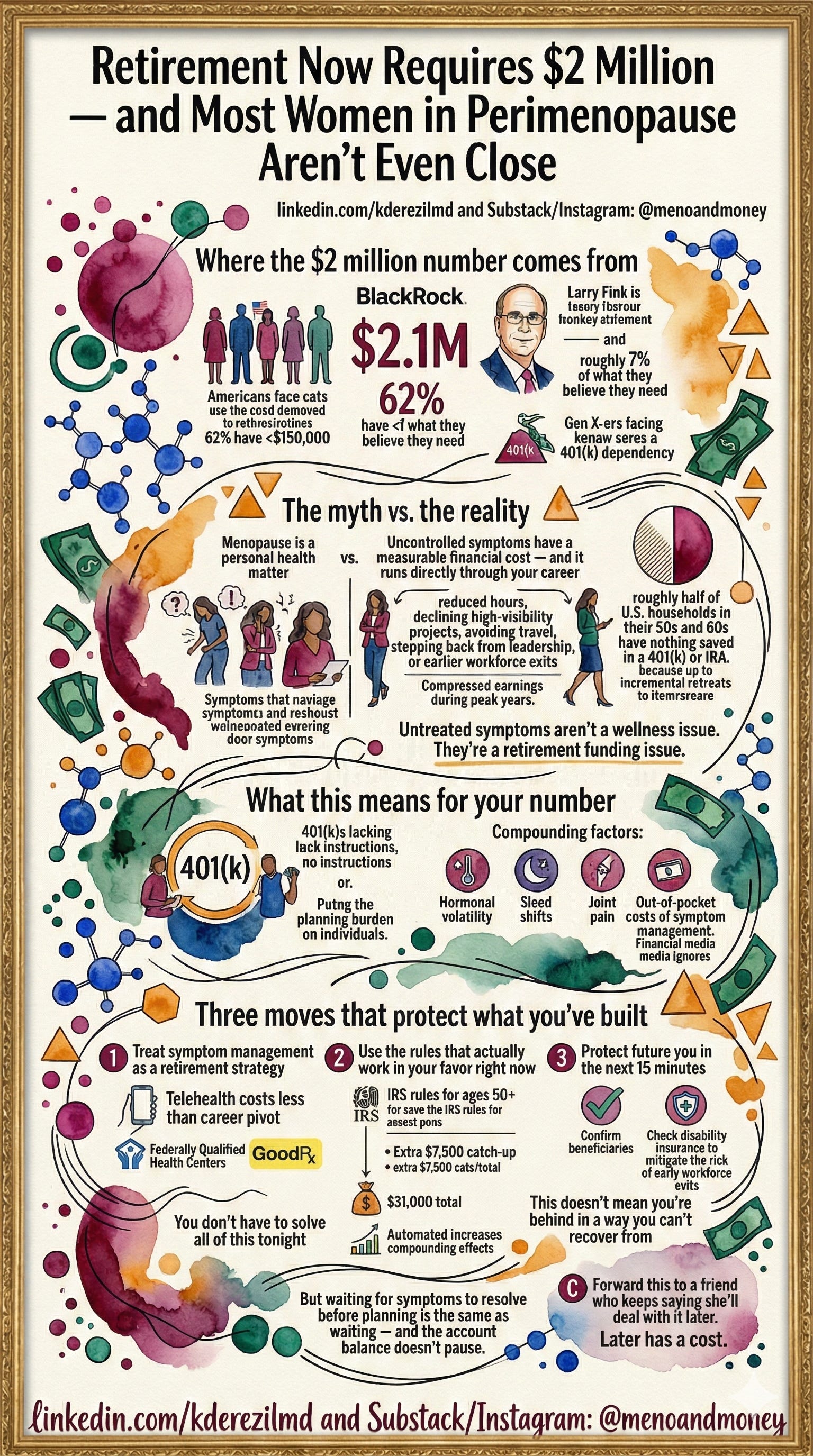

Where the $2 million number comes from

BlackRock — the world’s largest investment firm, managing $14 trillion — recently surveyed 1,000 Americans and asked: how much do you need to retire comfortably? The average answer was roughly $2.1 million.

BlackRock CEO Larry Fink called that number sobering — and noted that almost no one is close, given that 62% of those surveyed had less than $150,000 saved. That’s roughly 7% of what they believe they need.

This isn’t a Gen Z or Boomer problem. Fink specifically warned that the problem will get harder as the oldest Gen X-ers start to retire — the first generation primarily dependent on 401(k)s, with no employer pension safety net.

That’s you. And the transition hitting you right now is quietly making the gap wider.

The myth vs. the reality

Myth: Menopause is a personal health matter. Handle it privately and move on.

Reality: Uncontrolled symptoms have a measurable financial cost — and it runs directly through your career.

Women experiencing significant menopause symptoms are more likely to reduce hours, decline high-visibility projects, avoid travel, step back from leadership opportunities, or exit the workforce earlier than planned. Each of those decisions compresses earnings during what should be peak accumulation years.

Meanwhile, roughly half of U.S. households in their 50s and 60s have nothing saved in a 401(k) or IRA — and many of them arrived there through incremental retreats, not a single dramatic mistake.

Untreated symptoms aren’t a wellness issue. They’re a retirement funding issue.

What this means for your number

Even people who have saved face a separate problem: 401(k)s don’t come with instructions. Fink argues they’ve failed as a mass retirement solution because they put the entire burden of planning on the individual.

Add hormonal volatility to that burden — sleep disruption, mood shifts, joint pain, the sheer cost of managing symptoms out of pocket — and you have a compounding equation that financial media ignores entirely.

Three moves that protect what you’ve built

Treat symptom management as a retirement strategy, not optional spending. Telehealth menopause specialists cost far less than a career pivot or early exit. If cost is a barrier, Federally Qualified Health Centers offer income-based care, and GoodRx can reduce prescription costs significantly.

Use the rules that actually work in your favor right now. If you’re 50 or older, current IRS rules allow an extra $7,500 in catch-up contributions to your 401(k) this year — on top of the standard limit. That’s $31,000 total. Automate the increase today. Even 1% more makes a compounding difference.

Protect future you in the next 15 minutes. Log into one retirement account and confirm the beneficiary is current. Not a name from a decade ago. Then check whether you have disability insurance — because leaving the workforce early due to unmanaged symptoms is a real risk, and the financial gap it creates is preventable.

You don’t have to solve all of this tonight.

This doesn’t mean you’re behind in a way you can’t recover from.

But waiting for symptoms to resolve before planning is the same as waiting — and the account balance doesn’t pause.

“Uncontrolled symptoms aren’t a wellness issue. They’re a retirement funding issue.”